Network Tokens

Understand the benefits of Network Tokens.

Overview

Our recurring payments are enhanced by Network Tokenization.

A Network Token is a 16-digit value generated by the card schemes and it's used to replace the PAN in almost all parts of the payment process. Network Tokenization aims to enhance security, maximise conversion and potentially reduce costs for merchants processing recurring payments.

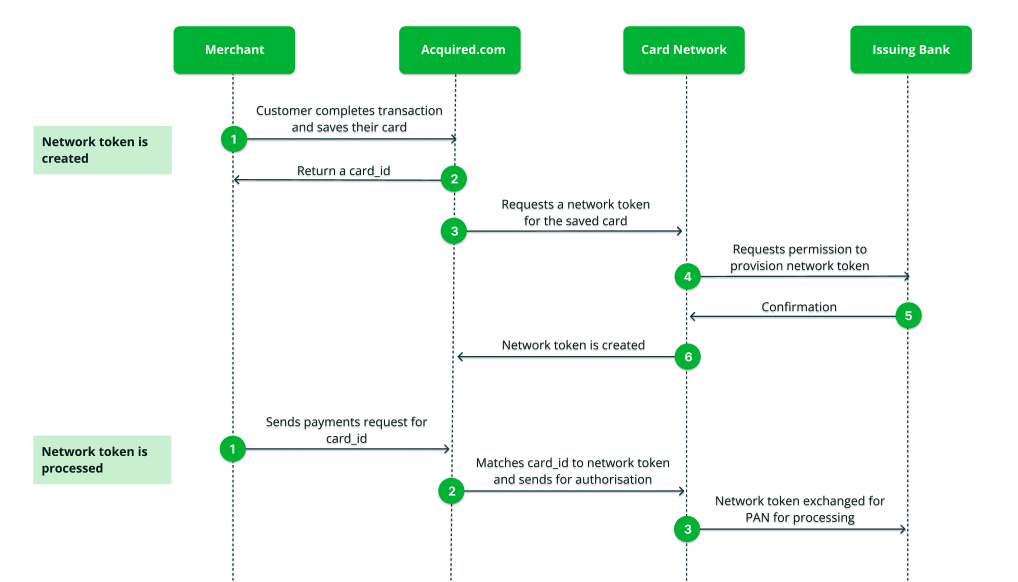

How does it work?

After you create a card, Acquired will request a network token on your behalf from the card scheme. Next time you submit a recurring payment for the card_id, Acquired will send the network token to the acquiring bank instead of the PAN. The network token is used right up until the transaction reaches the issuing bank where it is finally matched to the PAN for authorisation.

In rare instances, a network token creation request may be unsuccessful. If we can’t create a network token for a customer's card, the PAN will continue to be processed as normal.

The status of a network token can change, it will always be one of the following:

| Status | Description |

|---|---|

| Active | Network token is ready to be used for processing recurring transactions |

| Suspended | The issuer has suspended the network token, Acquired will use the original PAN to process transactions while the token is in this status. |

| Deleted | The issuer has deleted the network token, Acquired will process all further payment attempts using the PAN. |

The network token status can change from active to suspended, and back to active again. However, once a network token is deleted, the status will not change.

Leveraging our integrations with the card schemes, one of the key benefits of using our Network Tokenization service is the ability to keep card details up-to-date. If a customer's card is lost, stolen or expired, the token is updated in real-time and can continue to be used without asking the customer to update their payment information.

Ready to enable Network Tokenization? Contact our support team via our portal.

Network Tokens FAQs

What is network tokenization, and how does it benefit my business?

Network tokenization is a security feature provided by card networks like Visa and Mastercard. It replaces sensitive card data, such as the card number, with a unique token in all parts of the payment process. If a customer's card is lost, stolen, or expires, the network token remains usable and will update with the new card details in real-time. For merchants processing recurring payments, it means enhanced security, better conversion, and potentially reduced costs.

Is network tokenization supported for all transactions?

Acquired.com supports network tokenization for recurring Visa and Mastercard debit and credit card transactions. This includes both merchant initiated recurring payments, and returning customers paying with a stored card, across the majority of our acquiring partners. Please contact our support team to check if your current acquiring connections can support network tokenization.

Does that include digital wallets?

No, digital wallet transactions such as Apple Pay and Google Pay already utilise token capabilities. Additional network tokens are not created, or processed, for digital wallet tokens.

Do I need to make any changes to my existing payment processing setup to use network tokens?

No additional integration efforts are required. Built on our integrations with the card networks, unless you opt-out, Acquired.com handles the tokenization process seamlessly in the background.

How are network tokens created?

When a new card is saved for future use, 3-D Secure is completed as usual and the transaction is sent to the acquiring bank for authorisation. Following successful authorisation, Acquired.com requests a network token directly from the card network which is used for future recurring transactions.

Can I still use my existing stored tokens for recurring payments?

Yes, you can continue to use your existing tokens stored with Acquired.com. We will create network tokens for you in the background so you can continue to send recurring payment requests as normal.

Will my customers notice any difference when making payments with network tokens?

No, the customer experience remains the same. Customers will still use their cards as usual and they won't notice any difference in the payment process. Behind the scenes, their card data is tokenized for added security.

Is network tokenization mandatory, or can I choose to opt out?

While network tokenization is not mandatory, it is highly recommended for enhanced security. If you would like to opt-out, please contact our support team via our service desk to ensure the functionality is disabled on your account.

Are there any additional costs associated with using network tokenization?

Acquired.com charges a fee each time a new network token is created. There are also new scheme fees, which may be charged to you by your acquirer:

Visa Digital Credential Update Fee: $0.12 USD charged for the first attempted transaction following a token update. (new underlying PAN or expiry date)

Visa Non Secure Fee: Additional 0.025% applied to each Merchant Initiated Transaction that is processed without a network token.

How does network tokenization improve security for my business?

Network tokenization replaces cardholder data with a unique token. The tokenized data is useless to potential attackers because the token cannot be used elsewhere. This significantly reduces the risk of data breaches and fraud associated with storing card information. This solution is especially valuable for businesses dealing with online and card-not-present transactions, by reducing chargebacks and losses due to fraud.

How does network tokenization improve success rates?

Acquired.com’s existing gateway tokenization involves the exchange of tokens between merchants and our gateway. Network tokenization extends its reach to include acquirers and card issuers as well. After the card networks generate network tokens, they are shared with the issuers who gain better insight of token related activities happening between the consumer and the merchant. This increased understanding helps issuers feel more confident when deciding whether to approve transactions, which ultimately leads to higher authorisation rates.

How does network tokenization potentially reduce costs?

Visa has announced an increased cost of acceptance for non-tokenized merchant initiated transactions. Merchants processing recurring payments can offset the financial impact by enabling network tokenization.

What happens if a customer's card is reissued or expires?

If a customer's card is reissued or expires, the card network will send us a notification and the token remains usable. Acquired.com automatically associates the new card details with the token so you don’t have to ask your customers to update their payment information. This avoids declined payments and ensures continuity for customer transactions.

How can I receive the updated card details?

Utilise our card_update webhook to get notified when there are updates to a network token or its underlying card data.

Do I still need to use Account Updater?

Network tokenization is a robust solution for handling card updates, it securely manages the transition from old to new card information without any interruption to payment processing. If, in rare instances, a network token cannot be generated for a customer's card and you wish to retain Account Updater as a precautionary measure, please inform us.

I've enabled network tokens, why am I still receiving expired and lost card declines?

Acquired.com requests network tokens directly from the card network. In rare circumstances, the cardholders issuing bank may decline the request to create a network token and the card will continue to be processed as normal. Unfortunately this means we can not receive automatic credential updates and you may experience declines due to the card information being out of date. If you'd like to discuss utilising our legacy Account Updater product for such scenarios, please get in touch.

Updated 11 days ago